Prepare to raise | CORE

Expert guidance, investor matching, and visibility

Private rounds

Raise from your network with professional infrastructure

Cap table & equity management

All-in-one equity and stakeholder management

ESOP

Incentivize your employees and manage ESOPs seamlessly

Explore SeedBlink Legal

Subscribe to our newsletter

Share this term

How RSUs fit into compensation packages

Companies often utilize RSUs as part of a complete compensation plan to attract, reward, and retain top talent. For startups and large corporations alike, they offer a way to give employees a direct stake in the company’s success without the upfront cost of stock options.

Unlike stock options, RSUs don’t require employees to purchase shares at a set price; the shares are simply granted once they vest. RSUs can complement a salary and bonus structure by tying part of an employee’s reward to the company’s long-term growth. This not only motivates employees to stay until their units vest, but also helps align their interests with shareholders and the company’s overall performance.

RSUs are one of several tools companies can use to share equity with employees and build a culture of ownership, alongside Employee Stock Option Plans and Phantom Share schemes, which are especially common in Europe.

For many employees, RSUs (Restricted Stock Units) are the first form of equity compensation they receive. One of the most important things to understand is that the grant value shown in your offer or compensation package is not guaranteed cash. The actual value you receive depends on the company's stock price when the shares vest.

Since RSUs typically vest over several years, the value can increase or decrease over time, and any unvested shares are generally forfeited if you leave the company before they vest.

Another area that often catches people by surprise is taxes. In most cases, RSUs are taxed as income when they vest, even if you choose not to sell the shares. Depending on your location and tax situation, you may owe additional taxes later on any gains realized after vesting. It's also worth considering how much of your overall financial picture is tied to your employer. Your salary, bonus, and job security already depend on the company, so holding a large amount of company stock can create additional risk.

Before making financial decisions based on your RSUs, take time to understand your vesting schedule, tax obligations, company trading policies, and what happens to unvested shares if your employment ends.

Like any form of equity compensation, Restricted Stock Units (RSUs) come with their own set of pros and cons. Understanding both sides helps employees see the bigger picture of how RSUs can impact their earnings and career choices.

Advantages

Disadvantages

No dividends until vesting – RSUs typically do not pay dividends until they are converted into actual shares. That means employees miss out on any dividend income during the vesting period.

If you’re new to equity compensation, the language around Restricted Stock Units can feel a little intimidating. Here are the most important terms to understand:

Restricted Stock Units follow a clear process with two important dates: the grant date and the vesting date.

The grant date is when a company awards RSUs to an employee. This award outlines the number of units granted and the vesting schedule that determines when the employee will earn them. At this stage, the employee does not yet own shares of stock.

The vesting date is the date when the RSUs are converted into actual company shares. On this date, the employee gains ownership of the stock and can usually sell or hold the shares, subject to any company trading policies. Vesting often occurs gradually according to a set schedule—for example, a four-year plan with a one-year cliff and monthly vesting thereafter.

In practice, the grant date defines the promise of future shares, while the vesting date marks the point at which the shares become the employee’s property.

Taxation is one of the most important aspects of Restricted Stock Units, typically happening in two stages: at vesting and at sale.

At vesting

When RSUs vest and convert into actual shares, employees incur a tax liability equal to the fair market value of the shares on that date. The tax implications vary by country, but in most cases, taxpayers must report this value as ordinary income for tax purposes in the year of vesting.

Some companies make this easier by automatically withholding taxes, often through a “sell-to-cover” method where a portion of the shares is sold to cover the tax bill.

At sale (capital gains)

If an employee later sells the shares, any difference between the vesting price and the eventual sale price is subject to capital gains tax. The rate depends on how long the shares are held; short-term gains are usually taxed more heavily than long-term gains.

Country examples:

Once your RSUs vest, it's important to understand that you now own actual shares of company stock and need to decide what to do with them. Some employees choose to sell their shares immediately, while others hold them in the hope that the stock price will increase over time. Neither approach is universally right or wrong, but it should be a conscious decision.

A common mistake is holding shares simply because they were received through compensation, without considering whether you would actively invest the same amount of money in that stock today.

You should also familiarize yourself with your company's trading policies and the process for selling shares through your brokerage account. Depending on your employer, there may be trading windows, blackout periods, or other restrictions that determine when you can sell. Before making any transactions, make sure you understand the tax implications. In many countries, RSUs are taxed as employment income when they vest, and any additional increase in value between vesting and sale may be subject to capital gains tax. Keeping records of vesting dates, share values at vesting, and sale transactions will make tax reporting much easier.

Finally, don't assume that holding shares longer automatically leads to better outcomes. While some employees benefit from stock appreciation, others end up with a significant portion of their wealth tied to a single company.

To see how Restricted Stock Units work in practice, let’s look at a simple example.

A tech company hires Maria and, as part of her form of compensation package, she is granted 1,000 RSUs on her start date. The grant comes with a four-year vesting schedule and a one-year cliff. This means that after her first year, 250 RSUs vest all at once. After that, the remaining 750 RSUs vest in equal monthly installments over the next three years.

On Maria’s one-year work anniversary, the company’s stock price is $20 per share. At the vesting date, the 250 vested RSUs will convert into 250 actual shares, worth a total of $5,000. This amount is treated as ordinary income and taxed accordingly.

Maria decides to hold onto her number of shares. Two years later, when she sells them at $30 per share, she pays capital gains tax on the difference between the original vesting price ($20) and the selling price ($30), which is an additional $10 per share profit.

This example illustrates how RSUs reward employees for staying with the company while also providing them with the opportunity to benefit from the company’s stock price rising over time.

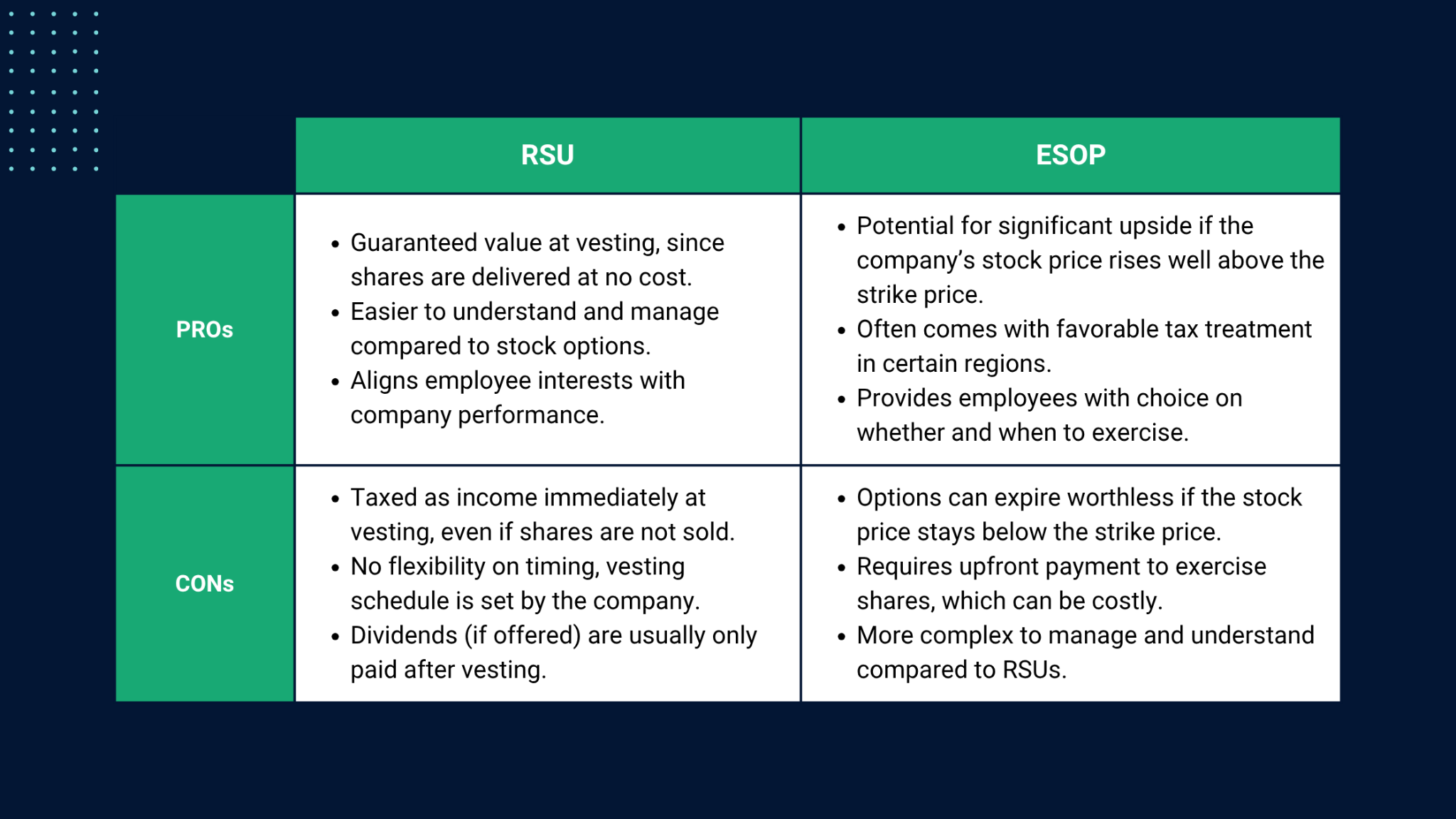

Restricted Stock Units (RSUs) and Employee Stock Option Plans (ESOPs) are two of the most common ways employees receive an ownership percentage in the company they work for. While both fall under the umbrella of employee compensation, they work differently and can create very different outcomes for employees.

RSUs are promises to deliver shares at a future date, while ESOPs give employees the right to buy shares at a fixed price, known as the strike price. Both approaches aim to reward employees for contributing to the company’s growth, but each comes with unique advantages and drawbacks.

The table below outlines the key advantages and disadvantages of RSUs and ESOPs.

1. Do RSUs always convert into shares, or can they be paid in cash?

Some companies settle RSUs in cash payments rather than stock, paying out the equivalent value of the shares at the time of vesting. This depends on the company’s plan.

2. Can I lose my RSUs if I leave the company?

Yes. Any RSUs that haven’t vested are typically forfeited when you leave. In some cases, companies may accelerate vesting for specific situations like layoffs, retirement, or a change of control.

3. What happens to RSUs if the company goes public or gets acquired?

If a company goes public, vested RSUs usually convert into publicly traded shares. In an acquisition, RSUs may be accelerated, canceled, or replaced with RSUs of the acquiring company, depending on the terms of the deal.

4. Do RSUs give me voting rights in the company?

Not until they vest. Employees don’t receive voting rights or shareholder privileges until the RSUs are converted into actual shares.

5. Do I have to pay tax on RSUs?

Yes. RSUs are typically taxed as employment income when they vest, and you may also owe capital gains tax on any increase in value between vesting and when you sell the shares.