Prepare to raise | CORE

Expert guidance, investor matching, and visibility

Private rounds

Raise from your network with professional infrastructure

Cap table & equity management

All-in-one equity and stakeholder management

ESOP

Incentivize your employees and manage ESOPs seamlessly

Explore SeedBlink Legal

Industry trends

Discover the latest fundraising insights in European venture that influenced the second quarter of 2025.

July 8, 2025

·

4

min read

%20-%20state%20of%20market%20pulse%202025%20-%20Q2.png)

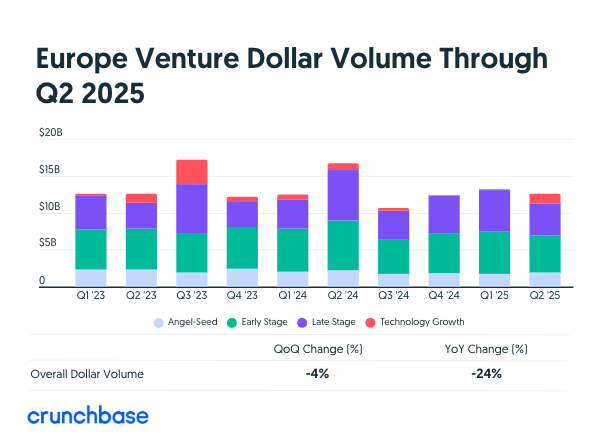

In Q2 2025, European venture capital funding came to a total of $12.6B, maintaining a similar level as the previous two quarters. While investment volume remained stable, overall deal activity declined, and fundraising slowed significantly. If the current pace continues, 2025 is projected to have the lowest annual fundraising total in a decade.

At the same time, some sectors and regions continued to show ongoing activity. AI, defence tech, and life sciences continued to attract capital, particularly at later stages. Southern Europe recorded notable deal growth, while countries like Germany and Israel led in large funding rounds.

In this article, we’ll have a breakdown of key metrics from the second quarter of 2025, including fundraising trends, regional performance, sector highlights, and more.

In Q2 2025, Europe’s venture funding totaled $12.6B, unchanged from the previous two quarters. Although overall activity remained steady, Q2 saw a 24% year-over-year drop. Since the 2022 downturn, quarterly funding levels have consistently ranged between $10B and $16B.

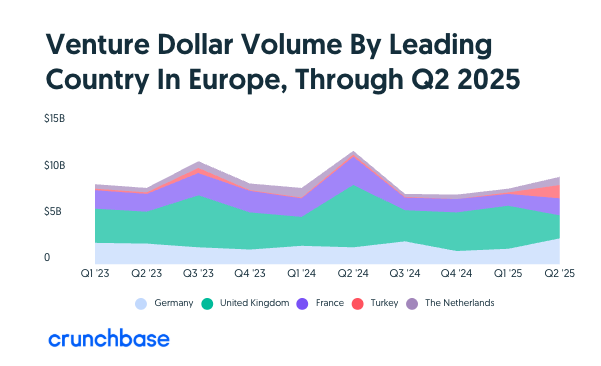

Germany led the region in total dollars invested for the first time since 2012, slightly ahead of the UK, which saw just $1.5B in Q2, its lowest quarterly total in over five years. France followed closely behind. The largest deal of the quarter was the round raised by Turkey-based mobile game developer Dream Games.

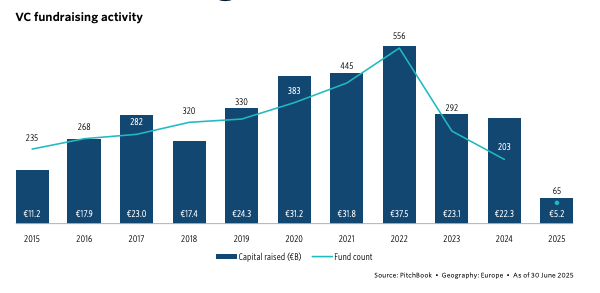

In the first half of 2025, VC fundraising in Europe reached €5.2B, putting the year on pace for a 53.1% decline compared to 2024. This would mark the lowest annual fundraising total in a decade. Only 65 funds closed in H1, continuing the downward trend from a peak of 556 in 2022.

The median fund size dropped to €50 million, the smallest since 2019. A growing share of capital is being allocated to emerging managers, with their portion increasing to 61.5% in 2025 from 43.5% the previous year. Despite some pending capital from open funds, slower distributions and broader economic uncertainty have delayed closings.

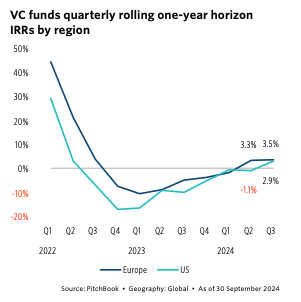

While venture capital performance has begun to recover from 2023 lows, returns remain subdued. As of Q3 2024, Europe’s one-year internal rate of return (IRR) stood at 3.5%, ahead of the US rate of 2.9%. Sector focus areas among these funds included energy, manufacturing, biotech, and healthcare. Overall, capital invested into European startups by these funds is showing signs of recovery, with investment multiples increasing to 5.6x in H1.

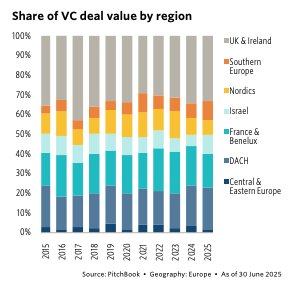

Funds from the DACH region (Germany, Austria, and Switzerland) surpassed the UK and Ireland in their share of European VC fundraising, accounting for 32.3% of total capital raised, up from 19% in 2024, in the first six months of this year. Germany alone contributed €1.2B, augmented by two €250 million raises from Picus Venture Fund II and Robert Bosch Venture Capital VI.

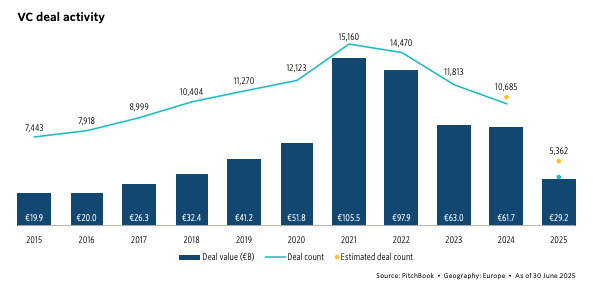

In the first half of 2025, European VC deal value reached €29.2B, with a 13% decline in Q2 compared to Q1. If this pace continues, the year could see a 5.3% drop in total deal value compared to 2024. The deal count also fell more sharply than the deal value, indicating reduced volume rather than diminished valuations. Volatility in global financial markets and investor caution likely contributed to a slowdown in dealmaking.

Private investors remain cautious, holding capital amid uncertain macroeconomic conditions. The data suggests fewer high-value transactions are happening during this uncertain period.

The continued influence of inflation and trade policy remains a key factor shaping market sentiment. Deal activity is distributed across all stages, with late-stage VC and venture growth consistently accounting for a significant share of the overall investment levels.

In Q2 2025, Southern Europe experienced an increase in VC deal activity, contributing to regional growth that exceeded 2024 levels. The region recorded €2.8 billion in deal value for H1, positioning it for a near two-thirds year-over-year increase. France & Benelux, on the other hand, recorded lower activity, with deal value decreasing 25.8% year-over-year in H1. The UK & Ireland maintained stable performance, reflecting broader market dynamics, while DACH remained active with a higher share of large-value deals.

Across Europe, early-stage activity showed the most resilience, accounting for a significant share of total deal value. Despite overall softness in volumes, deal sizes trended larger, with deals under €10 million still making up more than 80% of all activity.

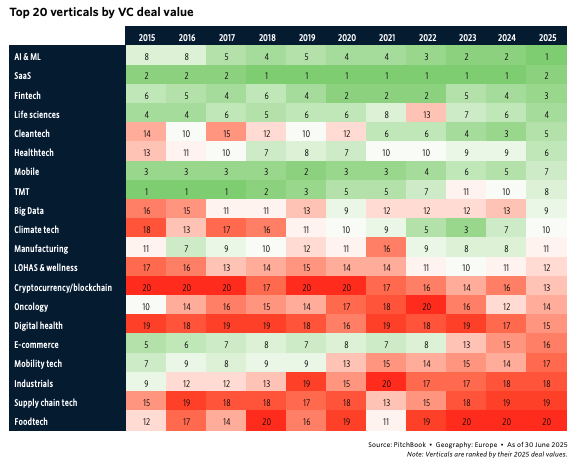

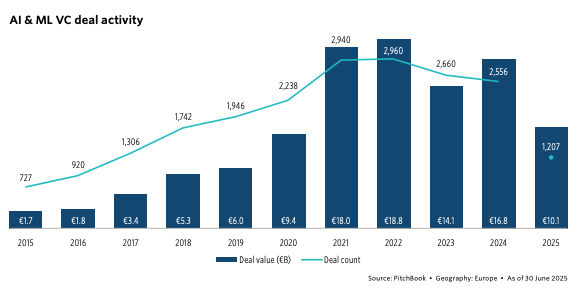

In H1 2025, AI and ML accounted for 34.5% of all VC deal value in Europe, totaling €10.1 billion. This trend of growth for the vertical has continued since 2021. However, its share still lags behind the 59.8% observed in the U.S.

Despite AI's strong presence in the data, much of the investment is concentrated in companies where AI is a feature within broader software offerings, rather than standalone technologies. This distinction raises questions about how AI-related businesses are classified and valued, especially as many rely on legacy software augmented with AI components.

Meanwhile, fintech and life sciences continued to show resilience and remained among the top-performing sectors, outpacing SaaS, which has seen softer deal flow in 2025. These two sectors, often associated with fewer but larger deals, have benefited from more stable market dynamics and steady investor interest.

Other sectors, such as climate tech and e-commerce, declined in ranking, reflecting a change in capital away from more volatile or cyclical verticals. So, investors seem to be favoring industries that have a business model that is easy to understand and able to generate consistent returns.

Despite the overall downturn, investment in defence and AI sectors remained active. Several of the largest rounds during the quarter were related to AI-powered defence technologies, with significant deals recorded in Germany, Portugal, Israel, and the UK. This indicates sustained investor interest in dual-use technologies, particularly at the intersection of AI and national security.

Governments across Europe also played a role in supporting the sector. The European Commission launched a €10B investment fund in Q2 2025, focusing on promoting critical technology capabilities. Meanwhile, Germany announced a separate €500M Defence and Infrastructure Fund. These public commitments align with increased VC funding in later-stage defense and AI startups, as investors have shown a reduced appetite for early-stage risk and responded to ongoing geopolitical and trade uncertainty.

In H1 2025, Berlin and Amsterdam recorded the highest concentration of AI-native funding rounds in Europe, according to Sifted, with 17.4% and 16.7% of deals, respectively, going to AI-focused startups.

These figures surpass those of traditional AI hubs, such as Paris (12.8%), London (11.9%), and Stockholm (8.8%). The reports indicate that Europe’s AI landscape is evolving, with emerging clusters across the continent attracting investor interest.

Secondary share sales are becoming increasingly common in venture rounds, particularly in Europe, as companies and investors seek ways to generate liquidity amid a prolonged slowdown in IPOs and M&A activity. Lawyers and market analysts have noted a growing piece of secondaries in later-stage deals, with some rounds including as much as 80% secondary shares.

The prolonged closure of the IPO window and muted exit activity have pushed more founders and shareholders to consider these sales as an alternative path to liquidity. Investors are also responding to this dynamic, with several firms launching dedicated secondary funds to acquire these stakes.

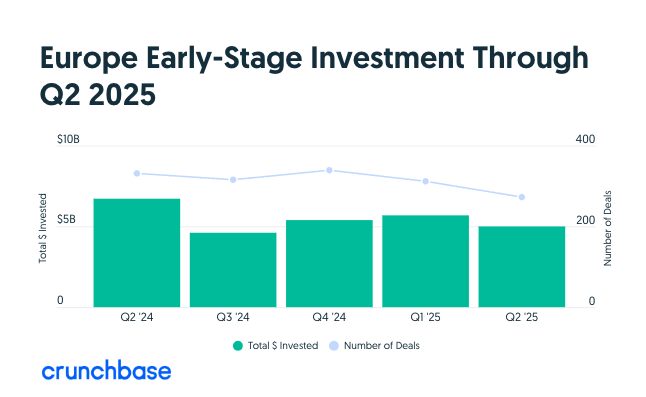

In Q2 2025, early-stage companies in Europe raised $5B across more than 270 funding rounds. This represented 19% of global early-stage funding. In comparison, North America secured $14.3B, accounting for just over a third of total early-stage funding.

The latest update from Crunchbase shows that Europe’s early-stage investment has remained relatively stable over the past five quarters, with total dollars invested fluctuating between roughly $4B and $6B, and the number of deals gradually declining from Q2 2024 to Q2 2025.

Worth mentioning here is that first-time venture financings in Europe have declined significantly since peaking in 2021, when $11.2B was invested across nearly 5,000 deals. By 2024, deal value had dropped to $6.2B, and the number of deals had fallen to just over 2,500. The trend is expected to continue in 2025, with a projected deal value of $3.6B and a deal count of fewer than 1,500.

In Q2 2025, European late-stage startups raised approximately $5.7B across 75 deals, accounting for about 10% of global late-stage venture funding. This was the smallest share among all funding stages.

The data from Crunchbase shows that while investment levels stayed consistent over the past five quarters, the number of deals slightly declined, with Q2 2025 seeing the lowest deal count during the period.

If you want to connect with VC funds or check out other active investors in the region, check out SeedBlink’s European VC Network list covering venture capital funds from SEE, DACH, Benelux, and others.

Written by

Patricia Borlovan

Communication Specialist

TABLE OF CONTENT

Subscribe to our newsletter

No spam. Just the latest releases and tips, interesting articles, and exclusive interviews in your inbox every week.

Share this article

The latest news, technologies, and resources from our team.

%20-%20Q1%202026%20-v2.2.png)

%20-%20Spain%20(angels%20%2B%20investors)%202.png)

%20-%20V1.4.2.png)

%20-%20Andrei%20Hancu%203.png)

%20-%20mir_detect.png)

%20-%20moneco%202.png)