Prepare to raise | CORE

Expert guidance, investor matching, and visibility

Private rounds

Raise from your network with professional infrastructure

Cap table & equity management

All-in-one equity and stakeholder management

ESOP

Incentivize your employees and manage ESOPs seamlessly

Explore SeedBlink Legal

All things equity

Can the EU-INC framework fix Europe’s fragmented VC landscape? Investors share what it could change for cross-border deals and syndicates.

April 3, 2026

·

5

min read

%20-%20eu%20inc.png)

Europe has long struggled with fragmentation in venture capital. Different legal systems, inconsistent deal structures, and varying levels of investor familiarity have made cross-border investing slower and more complex than it should be.

Now, the proposed EU-INC aims to change that.

After years of debate and growing pressure from founders, investors, and policymakers, the European Commission has moved to concrete proposals, signaling a more serious attempt to address these structural barriers.

If implemented effectively, it could introduce a truly unified framework for startups and investors across the EU, with elements like a centralized company register, cross-border stock option schemes, and more coordinated legal processes.

However, the recent draft and early reactions have also revealed considerable tension: while the direction of travel is broadly welcomed, many believe the current proposals still fall short of the original vision. Concerns remain about the continued reliance on national registries and courts, raising questions about whether the regime will truly deliver the level of standardization needed or simply streamline parts of an already complex system.

But what would this actually mean in practice? We asked investors across Europe to share their perspectives.

There is one theme that consistently comes up in investor conversations. It’s not a lack of capital; it’s a lack of clarity. Across Europe, investors are operating in a system where every cross-border deal introduces new layers of legal complexity, unfamiliar rules, and structural differences. Over time, this has created a hidden cost: hesitation.

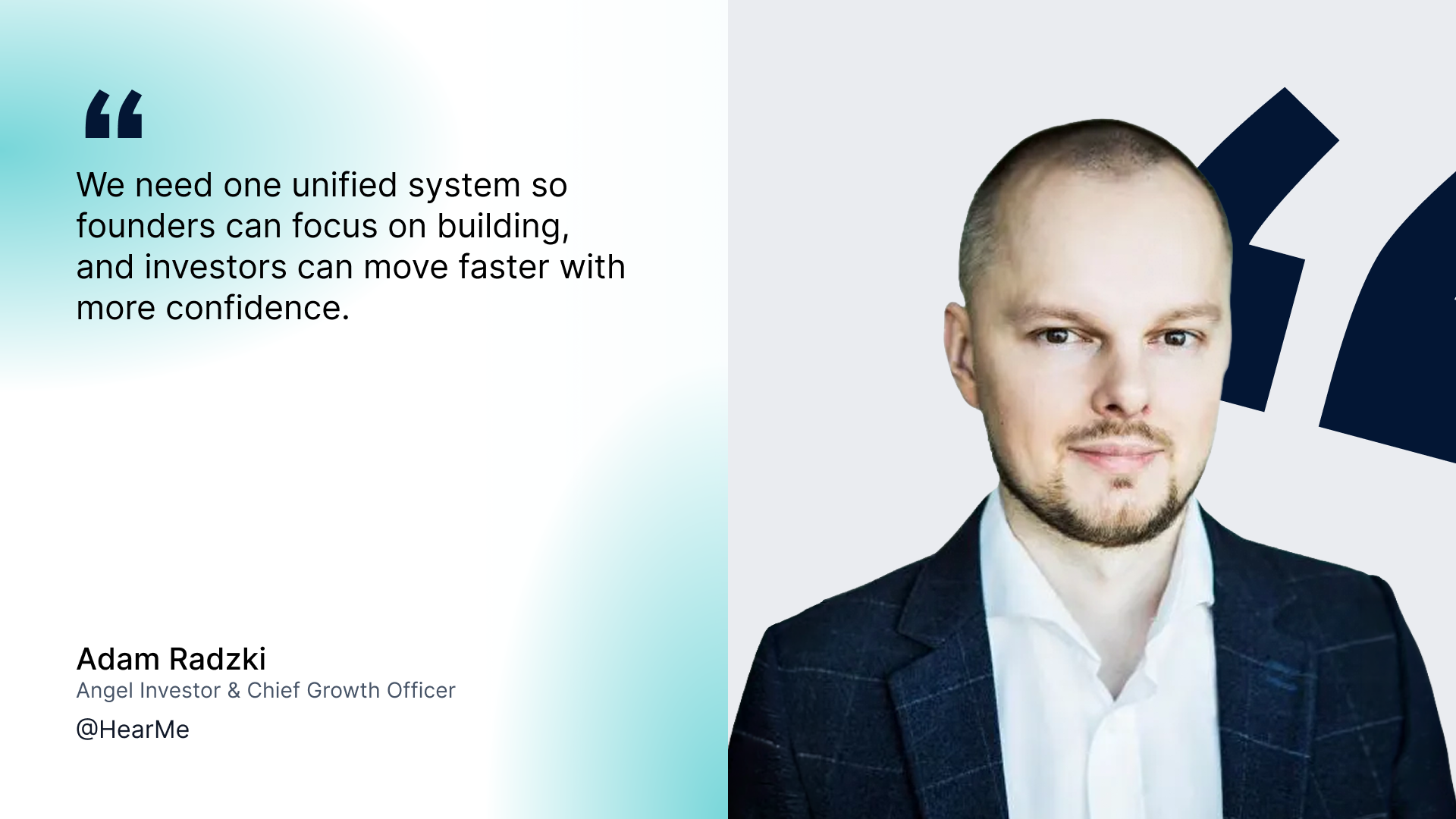

Adam Radzki, Angel Investor & Chief Growth Officer at HearMe, mentions:

This creates a “trust tax.” If EU-INC standardizes key elements, it will make deals faster, simpler, and more scalable across Europe.

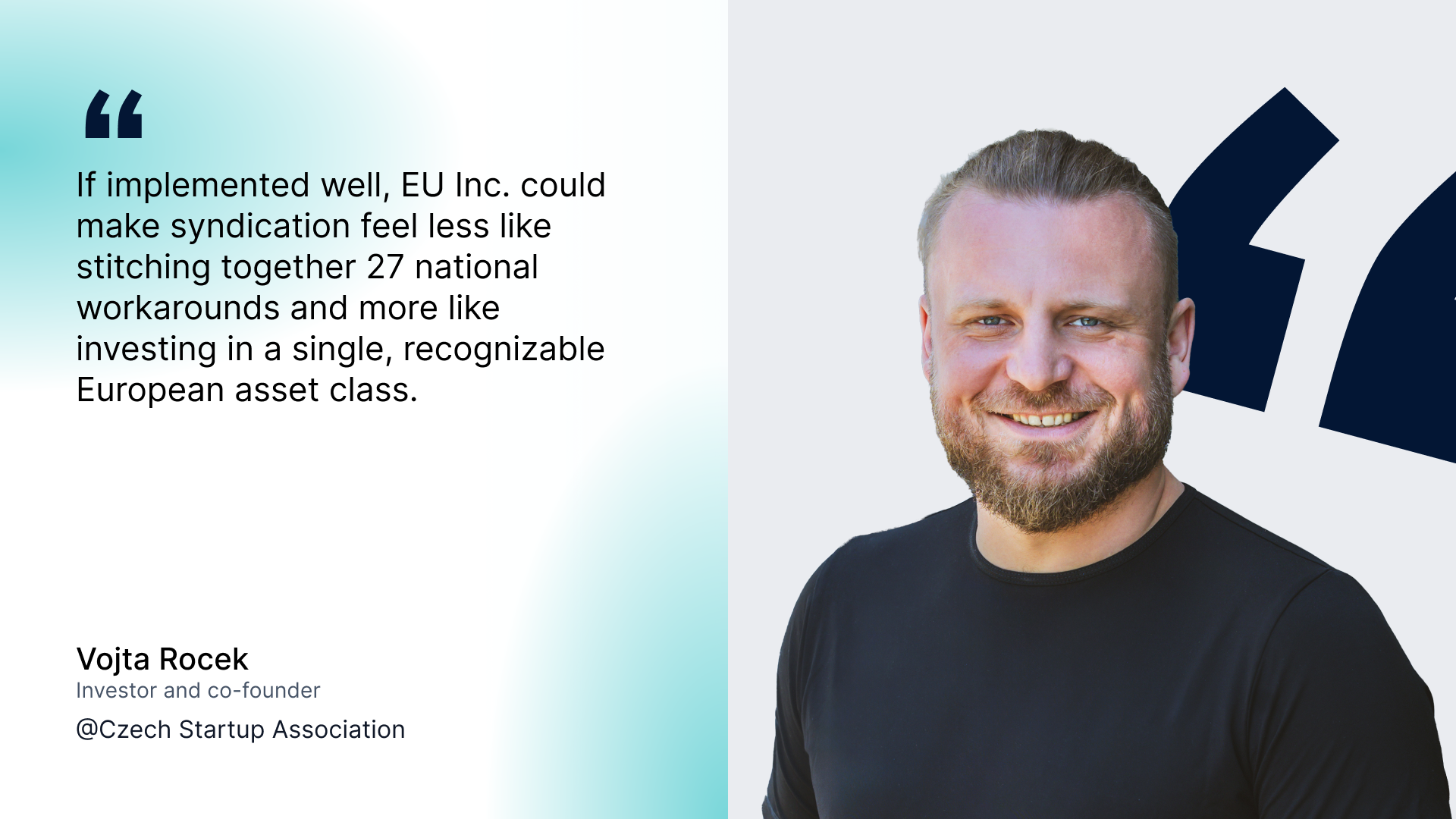

The thoughts are also echoed by Vojta Rocek, investor and co-founder of the Czech Startup Association, who says the potential impact could be significant, particularly for regions that depend on cross-border capital from day one.

EU Inc. could materially improve cross-border venture investing by standardizing the company being financed. One optional EU-wide company form – with digital incorporation, digital share issuances and transfers, no minimum capital, and SAFE-like financing logic – would make diligence, lead investor coordination, and syndication far more repeatable across borders.

But he also points out that standardizing startups is only part of the puzzle:

That said, EU Inc. is only half the equation. Europe is very good at standardizing the company and much worse at standardizing the capital behind it.

The Commission is already looking beyond EuVECA toward broader venture and growth capital reform – and that’s exactly the missing piece: a true ‘28th regime’ for VC itself. In simple terms, EU Inc. can standardize the startup; now Europe needs to do the same for the funds.

At the core of this hesitation is something more subtle than regulation itself: unfamiliarity. Even experienced investors tend to avoid markets where the legal and operational consequences aren’t fully understood, especially when those risks are hard to quantify upfront.

Petr Sima, Founder of DEPO Ventures, shares with us:

A single, unified regime could potentially eliminate this uncertainty and make investing across Europe as simple as a domestic deal.

These dynamics affect how investors support founders and how those build their companies. In many cases, the path to raising capital has meant stepping outside of Europe altogether.

Sarah Finegan, Associate Partner at Antler, also mentions:

EU-INC gives founders a genuine European alternative from day one: cheap, fast, and digital. If it works, more great companies will stay European, which is good for the whole ecosystem, including us.

Over time, this has led to a system in which the legal structure becomes an influencing factor rather than a neutral starting point. Founders optimize for investor familiarity, and investors gravitate toward jurisdictions they already trust, reinforcing fragmentation instead of reducing it.

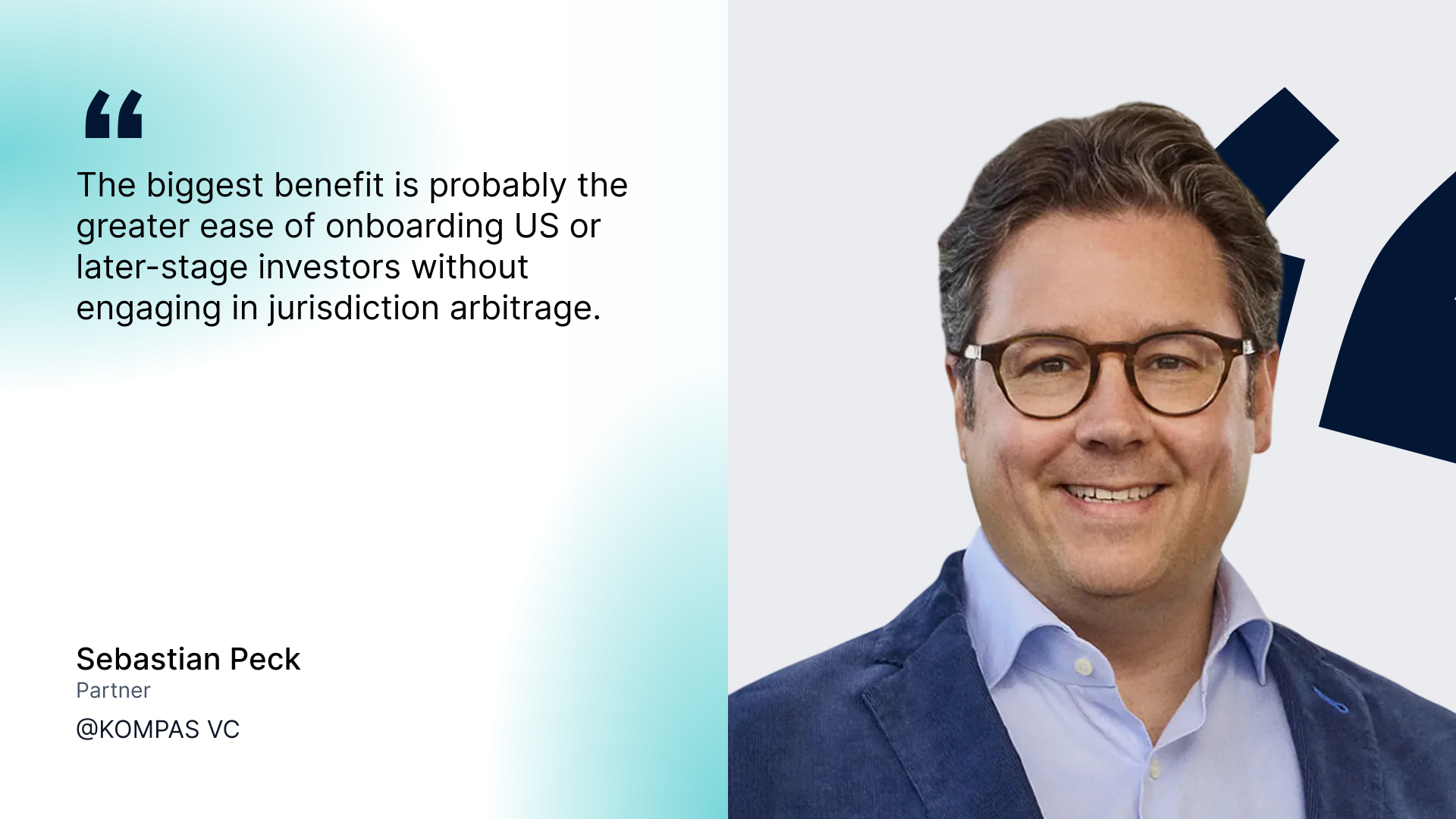

Sebastian Peck, Partner at KOMPAS VC, adds:

%20-%201920x1080%20(16_9)%20-%20vizual%206.png)

EU-INC directly addresses this by providing one standardized corporate structure and investment framework. It also enables fast, digital incorporation (48h) and ideally harmonises equity incentives, which is critical for talent retention.

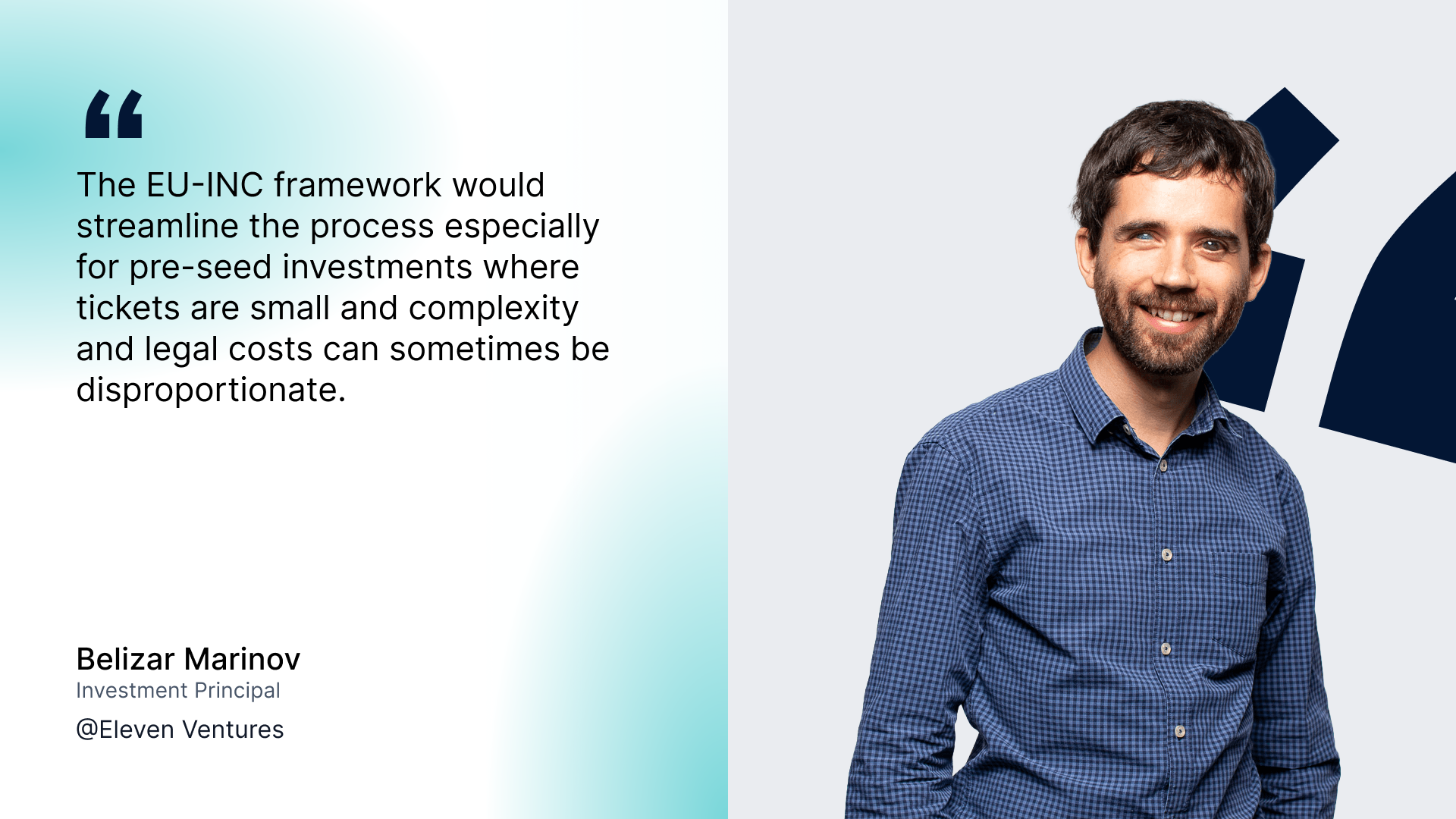

This complexity is felt most acutely at the earliest stages, where resources are limited and even small inefficiencies can have an outsized impact on founders.

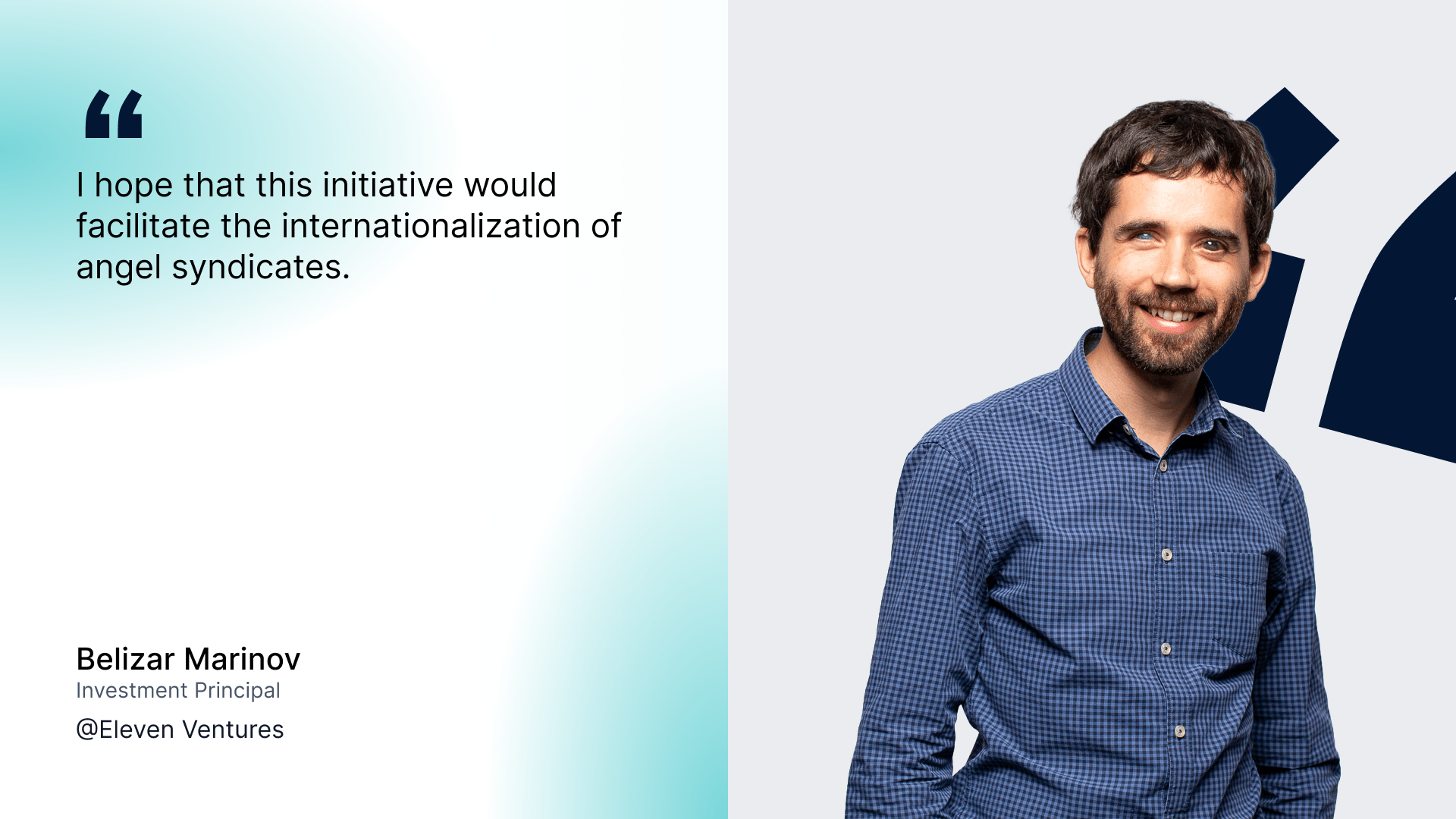

Belizar Marinov, Investment Principal at Eleven Ventures, adds:

I hope it will enable angel investors and micro VCs to have access to more international founders.

Today, Europe’s fragmented legal landscape slows deals down and adds uncertainty. A unified framework could change that by introducing shared standards, making companies easier to understand, and helping investors move with more confidence across markets.

For Vojta Rocek, investor and co-founder of the Czech Startup Association, the most immediate impact is at the company level, where much of Europe’s friction still sits.

Today, too many founders still need foreign holding structures – often in places like Delaware – or bespoke legal work just to become VC-compatible. Corporate forms, share mechanics, transfers, and early-stage instruments remain unnecessarily fragmented across Member States. EU Inc. goes straight at that layer.

It won’t fix Europe’s late-stage capital gap. But if founders no longer need to redomicile just to run a clean round, that alone is a meaningful shift – especially in smaller ecosystems, where legal friction is amplified by a thinner funding base.

Adam Radzki, Angel Investor & Chief Growth Officer at HearMe, also addresses this from a different point of view:

From an angel investor perspective, this should significantly ease investing across Europe.

Today, it’s very difficult to navigate the different legal systems across EU countries—each with its own rules, risks, and nuances. Time is life for startups, yet we lose a lot of time and money on fundraising and legal work.

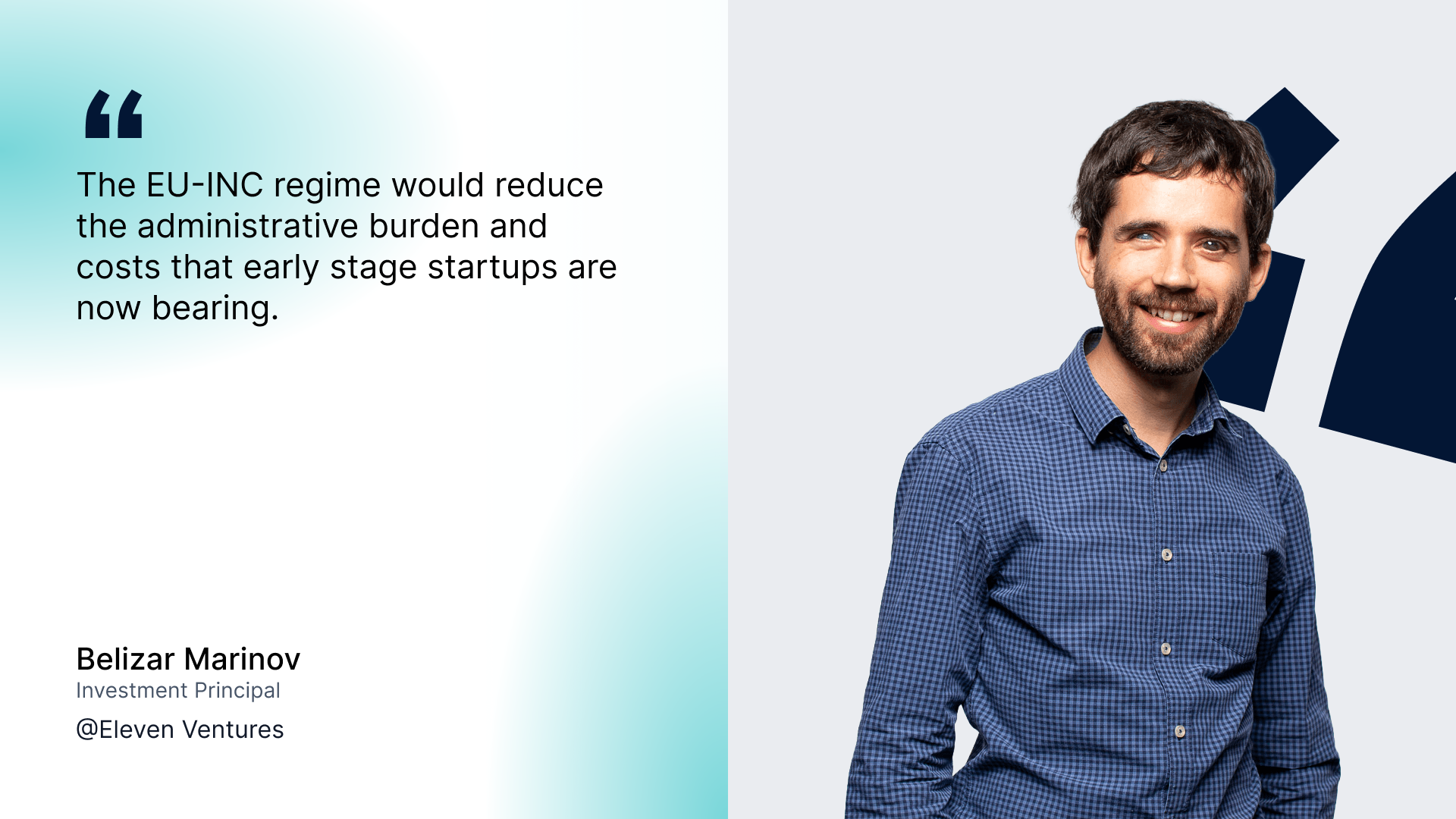

While much of the conversation focuses on system-wide efficiency, some of the most immediate benefits may be felt at the earliest stages of investing, where legal complexity often outweighs ticket size.

Belizar Marinov, Investment Principal at Eleven Ventures, underlines this dynamic:

Often times founders end up having multiple legal entities in various countries which can present an excessive expense when revenues are still limited.

VC investors are used to investing in various jurisdictions, but whether a certain jurisdiction is considered investor-friendly depends also on other factors outside of the EU-INC scope.

What emerges from early reactions is not just a desire for efficiency, but a recognition that fragmentation itself has been a strong constraint on the ecosystem’s growth.

Petr Sima, Founder of DEPO Ventures, adds:

Beyond an easier setup for investment structures, it may represent a shift toward a unified capital market. I hope it effectively increases trust in cross-border deals.

Ideally, it will allow us to focus on the invested companies rather than navigating the legal complexities of different jurisdictions.

Investors are optimistic about the intent, but aware that the real test will be in how the framework is implemented and adopted across markets.

Sarah Finegan, Associate Partner at Antler, also mentions the following expectations:

I am cautiously optimistic. The proposal just dropped, and there's political will to pass it this year.

As a UK investor, though, we're outside this. If anything, it might make European deals easier for Continental funds to lead, so we need to stay proactive about being in those syndicates rather than assuming we'll get called.

One of the more immediate effects of a standardized framework could be the change in perception. In venture, familiarity plays an important role in fundraising decisions. When structures are unfamiliar, investors tend to hesitate, especially in less mature or less internationally visible ecosystems.

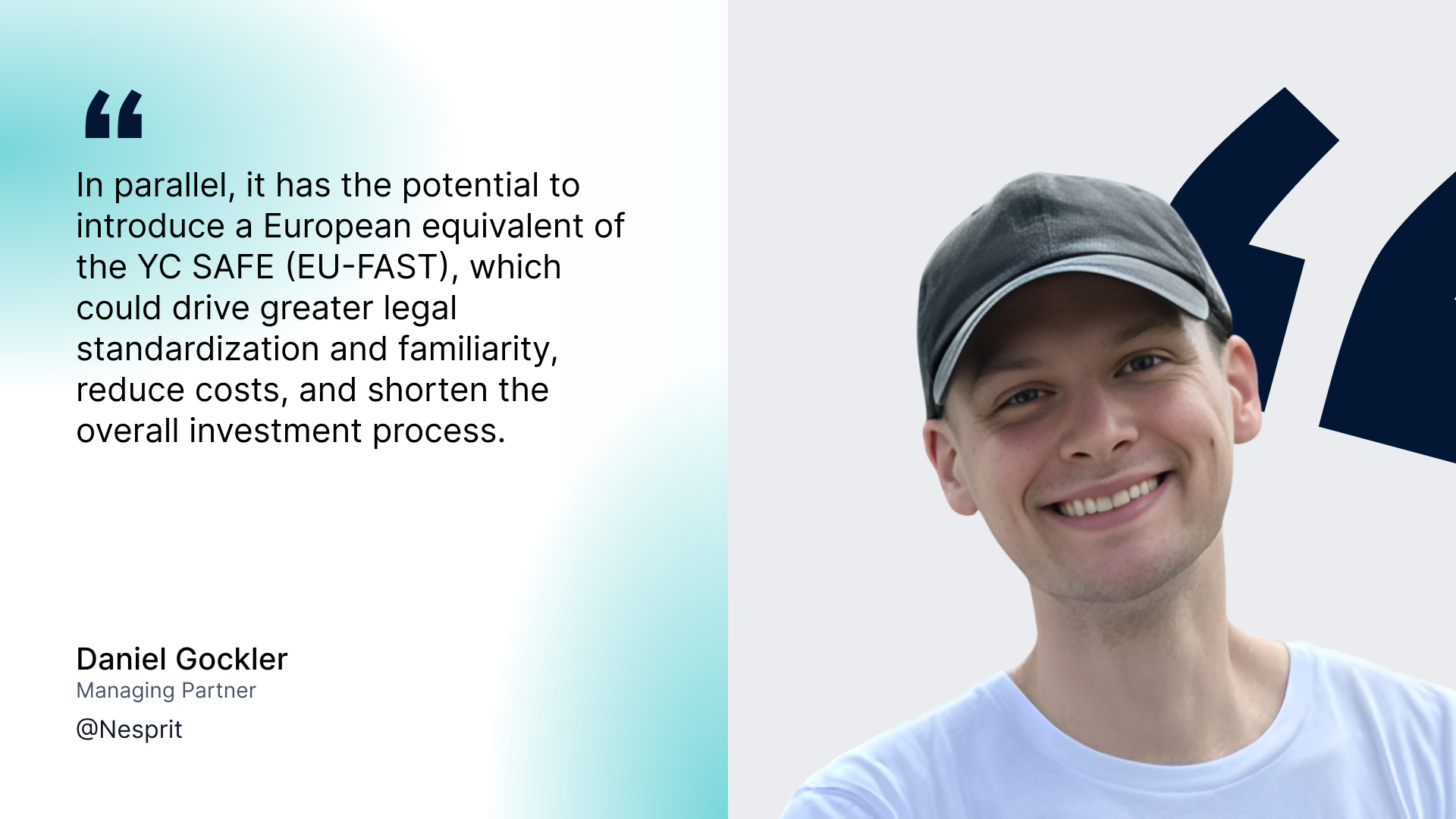

As Daniel Gockler of Nesprit mentions:

A shared structure could act as a common language, reducing friction between investors and making companies easier to evaluate at every stage.

Sebastian Peck, Partner at KOMPAS VC, also adds:

%20-%201920x1080%20(16_9)%20-%20vizual%2012.png)

It potentially makes European companies more legible to global capital, closer to a Delaware-like standard. While this would make things much simpler, labour law and taxation remain subject to national policies, so true single-market investing is still incomplete.

Syndication in Europe has never been limited by ambition, but by complexity. Bringing together investors from different countries often means navigating multiple legal systems, aligning different expectations, and managing added execution risk. As a result, many syndicates remain locally anchored, even when opportunities are inherently cross-border.

The EU-INC could begin to change that by introducing a shared framework, one that makes collaboration simpler, faster, and more predictable across markets.

Looking ahead, Vojta Rocek, investor and co-founder of the Czech Startup Association, believes the biggest change could be in how investors actually work together across borders.

Funds across Member States should be able to rely on shared assumptions around documentation, cap tables, digital closings, and follow-on mechanics – reducing execution risk and speeding up pan-European rounds.

But the real step change only comes if the fund side is fixed as well: less gold-plating, a better passport, simpler onboarding and KYC, and a solution to the €500m AIFMD cliff. The best outcome is straightforward: EU Inc. becomes the default vehicle for startups, and venture and growth capital reform becomes the operating system for the funds backing them.

Adam Radzki, Angel Investor & Chief Growth Officer at HearMe, also mentions:

It should help fund teams that are distributed across countries and support truly European companies—those that operate, hire, and pay taxes in Europe, while scaling across markets. This could lead to more cross-border syndicates and a more integrated European VC ecosystem.

For angel organizations and syndicates, this should significantly improve the ability to attract new angels; today we expect startups to operate globally from day one, and this structure should help enable that.

However, the impact may not be uniform across all stages. While larger funds already operate across jurisdictions, the most meaningful shift could happen earlier in the funding lifecycle.

Belizar Marinov, Investment Principal at Eleven Ventures, adds:

I don't see it having a major operational impact on VCs per se, but it can foster improved investment flows in the pre-seed stage, which would position startups better with institutional investors.

Today, syndicates often form within familiar networks, where investors share legal context and operational understanding. A unified structure could expand those circles, making it easier to collaborate beyond domestic markets.

Petr Sima, Founder of DEPO Ventures, adds:

Ideally, it will also bring much-needed clarity through a single regulation for syndicates, making it a simpler process to invest with funds from other countries.

In practical terms, this could simplify how deals come together. Instead of stitching together different systems, investors could operate from a common baseline, reducing friction at every step of the process.

Sarah Finegan, Associate Partner at Antler, also mentions:

A shared company structure means everyone works from the same playbook, standard docs, shared expectations, and achieves quicker closes. The big "if" is whether the actual legal templates are flexible enough for real VC deals (multiple share classes, options, convertibles). That detail hasn't been decided yet, so the jury's still out on whether this is genuinely transformative or just tidying up admin.

Standardization could also extend to the tools and instruments used in early-stage investing.

As Daniel Gockler of Nesprit mentions:

Beyond Europe, this change could make the region more accessible to global capital. A shared structure would make it easier for international investors to join syndicates without requiring companies to restructure or relocate.

Sebastian Peck, Partner at KOMPAS VC, also adds:

Standardized docs also reduce negotiation overheads between funds in different jurisdictions and remove the need to anchor deals in a specific legal system, which could encourage more European funds to lead rounds outside of their own jurisdiction. That said, local biases will likely persist (networks, sourcing, regulatory familiarity).

Also, late-stage capital constraints remain the major bottleneck in Europe that requires a whole set of different policy changes.

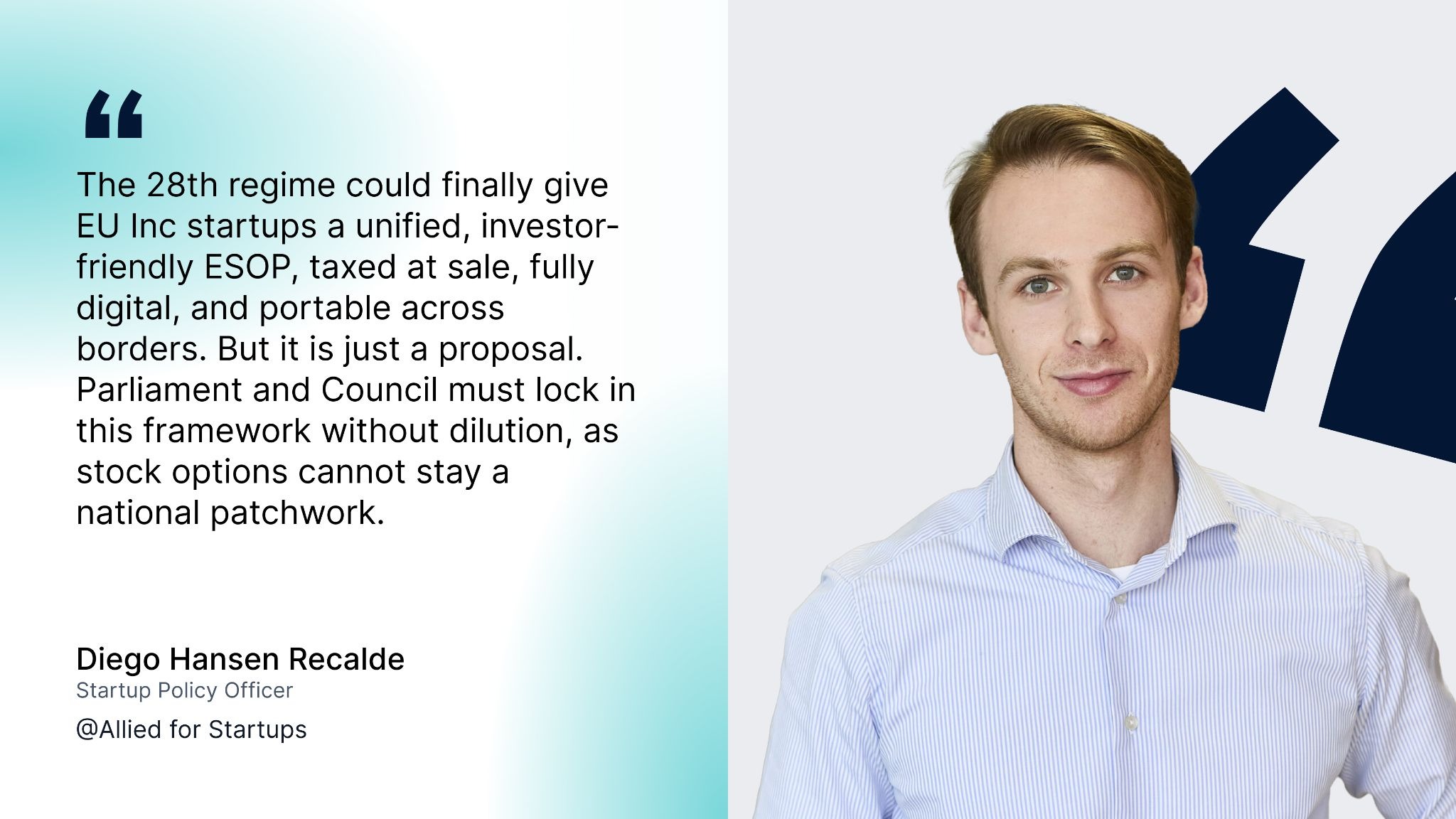

Beyond deal structures and syndication, one area where fragmentation is especially visible is employee equity. Today, stock option frameworks vary significantly across countries, making it harder for startups to attract talent, scale teams across borders, and compete globally. The EU-INC has the potential to address this by introducing a more unified, startup-friendly approach to ESOPs at a European level.

As we hear from Diego Hansen Recalde, Startup Policy Officer at Allied for Startups, who has worked on this file both within the European Commission, and now from the ecosystem side.

"Working on this file in Brussels, the momentum is real: the 28th regime could finally give EU Inc startups a unified, investor-friendly ESOP, taxed at sale, fully digital, and portable across borders. But it is just a proposal.

The cheerleaders for making Europe a place to start, grow, and succeed must push hard to ensure maximum ambition"

If EU Inc delivers on its promise, cross-border investing could become faster, simpler, and far more repeatable. But execution will still matter. Investors who can move quickly, collaborate across markets, and structure deals efficiently will be best positioned to benefit from this change.

That’s where infrastructure becomes a real advantage. Whether you’re an angel, operator, or fund looking to lead deals across borders, having the right tools can make the difference between momentum and missed opportunities.

With SeedBlink, you can launch and manage your own syndicate without the usual operational challenges, bringing your network together, structuring deals on your terms, and focusing on what actually matters: backing great founders. If you’re ready to turn insight into action, now is the moment to start building.

Written by

Patricia Borlovan

Communication Specialist

TABLE OF CONTENT

Subscribe to our newsletter

No spam. Just the latest releases and tips, interesting articles, and exclusive interviews in your inbox every week.

Share this article

The latest news, technologies, and resources from our team.

%20-%20part%204.0.png)

%20-%20part%203.2.png)

.jpg)

%20-%20part%202.png)

%20-%20part%201.png)